Just remember that most homeowner’s insurance policies won’t cover flood damage, so contact your flood insurance company if your home has flooded. If you don't have flood insurance, you might be stuck paying for the damage yourself.

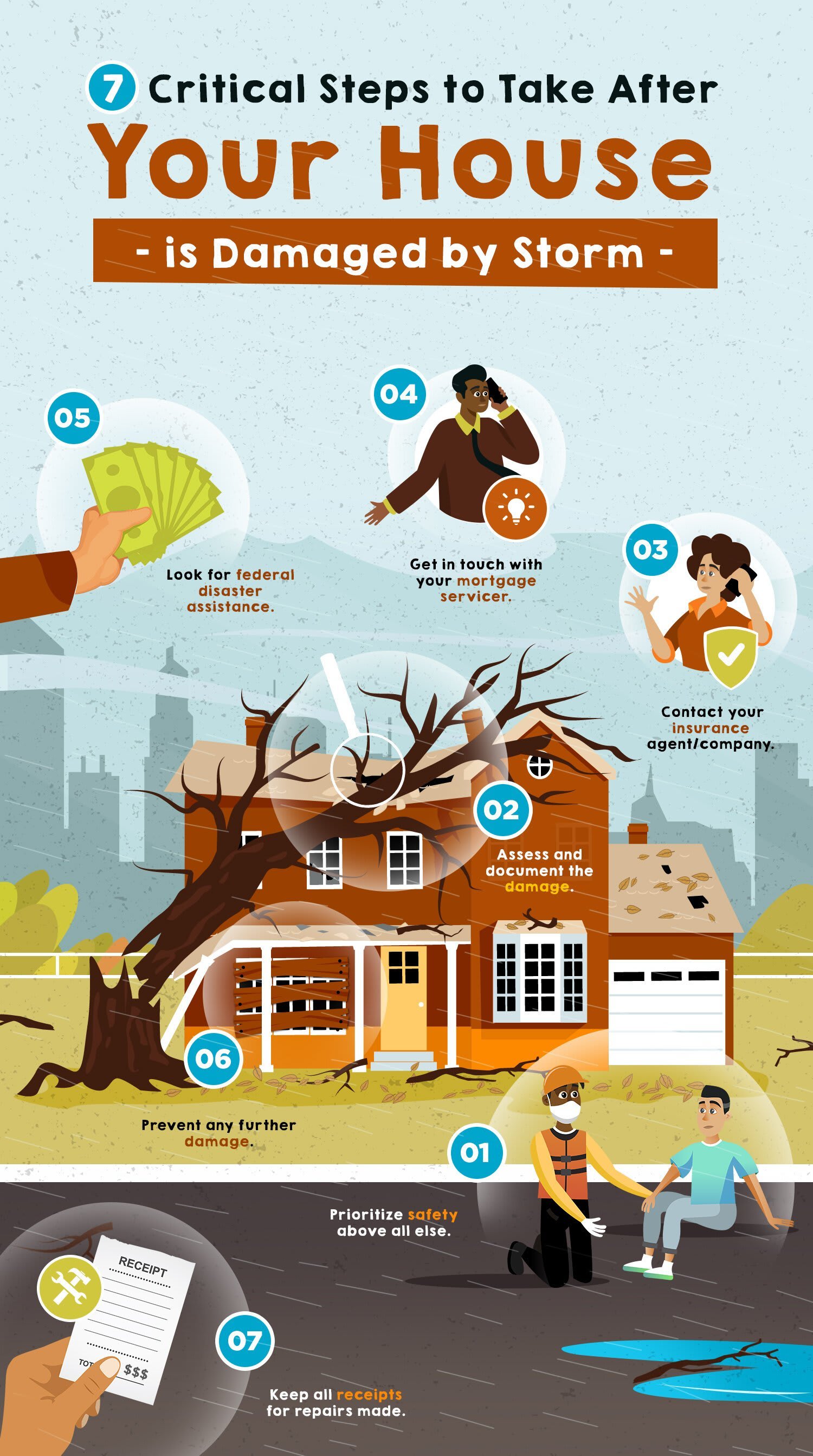

4. Get in Touch With Your Mortgage Servicer.

Aside from your insurance company, you should also contact your mortgage servicer—the company you send your monthly mortgage payments to (it might not be your original mortgage lender), as soon as possible to talk about available mortgage relief options.

If the disaster makes it difficult or even impossible to make your monthly house payments, make sure you talk with your mortgage servicer first to avoid being charged late fees, which could cause your credit score to fall. Ask if they could offer mortgage forbearance, which allows you to make partial payments or stop making your payments for an agreed-upon time. A forbearance usually lasts up to six months and can be extended up to another six months.

5. Look for Federal Disaster Assistance.

The Federal Emergency Management Agency (FEMA) provides a variety of assistance to homeowners who were affected by storm damage. You can get help with temporary housing, repairs, meals for your family, and filing insurance claims. If your area was declared a storm disaster area, you may be eligible for low-cost loans to help restore your property back to normal. Even if you do have a solid insurance policy, you may still qualify for more federal disaster assistance. You will be required to file documents in order to receive these loans.

6. Prevent Any Further Damage.

Once you're sure the storm has passed, you can start cleaning up the debris and do a few necessary emergency repairs to stop any further damage from occurring. Just remember to do it as safely as possible, and try not to make any extensive and permanent repairs before an insurance adjuster has had a chance to assess the damage.

Remove any debris from your yard, deck, and patio, and even from the roof and gutters. If there are holes in your roof or your windows are broken, be sure to cover them as quickly as possible so that wind and rain do not seep in. Make sure the downspouts are working to keep water away from your foundation and property. If there’s clogged or standing water somewhere, try to get rid of the clog on your own to prevent mold growth, which can be hazardous to you and your family’s health.

Your insurance agent could also help you contact a local restoration service provider who will aid in tackling storm damage and getting your property back to normal. Secure any valuable items that are at risk of being damaged while the restoration process is ongoing.

7. Keep All Receipts for Repairs Made.

Make sure to save all receipts for materials and labor, and keep records of all additional expenses. This is to ensure you receive fair reimbursement. Keeping good documentation and staying organized with your paperwork is critical for any claim to your homeowner's insurance to avoid headaches and potential problems later.

Familiarize yourself with what your homeowner’s insurance policy covers if your home is damaged by a disaster. Also, make sure you review and update your contact information with your insurance company.